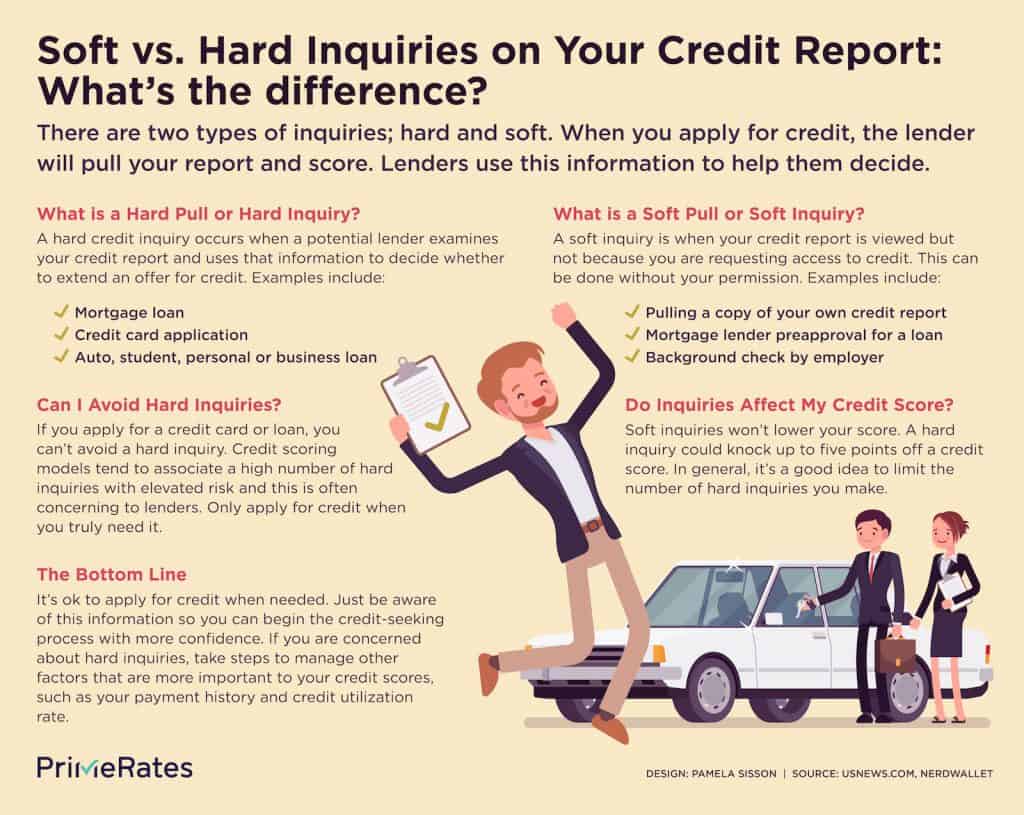

You may know that lenders often “pull your credit” when considering you as an applicant. But did you know that there are two types of credit inquiries — a soft credit inquiry and a hard credit inquiry?

Here’s the difference between a soft credit inquiry and a hard credit inquiry:

Soft credit inquiries

These may occur without your knowledge, but they don’t impact your credit score in any way. Here are some situations in which a company might do a soft credit pull:

- Background checks

- Mortgage loan preapprovals

- Credit card offers in the mail

Checking your own credit also falls under the “soft inquiry” category. By law, you’re entitled to one free credit report from each of the three major credit bureaus per year. You can pick them up at annualcreditreport.com.

Hard credit inquiries

These occur when lenders examine your credit report to fully evaluate you as a candidate for lending. Here are some situations in which a company might do a hard credit pull:

- Getting a mortgage loan

- Credit card applications

- Auto, student, personal or business loans

How inquiries impact your credit score

While soft inquiries won’t impact your credit score in any way, a hard inquiry can drop your score a few points. So in general, it’s a good idea to limit the number of hard inquiries you make.

But keep in mind that if you are “rate shopping” — looking for a mortgage, auto or student loan, for example — all inquiries you make within a 45-day window are considered one inquiry.

The bottom line

It’s best only to apply for credit when you really need it, otherwise you could ding your credit score.

But remember, things like checking your own credit, renting a car or signing up for internet fall under the soft credit inquiry umbrella.

Keep an eye on your credit by pulling your credit reports at least once per year, paying off your credit card bill in full each month and keeping your credit utilization ratio relatively low.